In a world where uncertainty is becoming increasingly prevalent, insurance companies play a key role in providing peace of mind and protection. Whether it’s to cover a car accident, a medical emergency, or a professional disaster, these players are there to secure our daily lives and our future. But do you really know how these companies operate and what services they offer to meet the diverse needs of citizens and businesses? In 2025, with the rapid evolution of risks and technologies, their range of services has expanded further, incorporating innovations such as cybersecurity and climate management. Giants like AXA, Allianz, and MACIF are trying to differentiate themselves with tailor-made offers, while mutual insurers such as GROUPAMA and SMACL favor a more community-based approach. With digitalization, they also offer more accessible online services, allowing everyone to manage their policies without leaving their home. Concretely, understanding the services offered by an insurance company is a step toward better risk management and tailored protection at every stage of life. It also means understanding how these companies contribute to strengthening the financial stability of our society while innovating to meet the new challenges of 2025.

Discover the structure and mission of insurance companies in France

An insurance company is, above all, an organization that manages risks for its clients in exchange for the payment of a premium. Its primary objective is to provide a safety net against life’s uncertainties. But what also differentiates an insurance company is its legal structure. In France, these companies must adhere to a strict regulatory framework, notably through the French Insurance Code, which guarantees transparency and stability in the sector. These firms can take several legal forms: public limited company, mutual insurance company, or mutual insurance company, for example. Each of these structures adheres to specific principles, such as the pursuit of profit or solidarity among members. The diversity of models also allows for the emergence of new offerings, adapted to market requirements and regulatory developments, particularly with the European Solvency II directive. The uniqueness of these companies lies in their ability to balance profitability and prudent risk management, while offering varied and innovative services to meet all expectations. And among them, players like ALLIANZ and GENERALI play a major role in this highly regulated landscape, combining financial performance and social responsibility.

The Main Categories of Insurance Companies in France and Their Role

In practice, we can distinguish between different families of companies that coexist in the French market. Understanding their specificities also helps us better understand how they influence our daily lives. Here is a clear overview of these players:

| Type of Company | Main Characteristics | Concrete Examples | Major Advantages |

|---|---|---|---|

| Insurance Companies (SA) | Commercial company with capital held by shareholders. Often listed on the stock exchange. | AXA, Allianz, and FONCIA provide a wide range of products, including auto and home insurance. | Ability to raise significant funds 💰, investing in technological innovation. |

| Mutual Insurance Companies | Companies without share capital, based on solidarity, democratically managed. | MACIF, Groupama, SMACL. Members have their say through voting. | Non-profit orientation, reinvestment in the quality of guarantees 🌿. |

| Mutual Insurance Companies (SAM) | Hybrid forms, combining aspects of a mutual and a commercial company. | Example: certain subsidiaries of ALLIANZ or GENERALI. | Increased flexibility, possibility of creating subsidiaries to diversify offerings. |

| Subsidiaries of foreign companies | Operate under the European system, often highly innovative. | Present in France, often with advanced digital strategies. | Diverse, competitive, and international offering 🌍. |

These different types of companies each contribute in their own way to addressing new challenges, such as cyber insurance or protection against climate disasters. Regardless, they all play a crucial role in the French economic and social fabric, ensuring stability and innovation.

The major role of regulation and supervision in insurance

The insurance sector, because it affects the stability of the entire economy, is heavily regulated by authorities to avoid systemic risks. In France, the ACPR, the Prudential Supervision and Resolution Authority, oversees the majority of players. It ensures that companies like SPOLÉA and FONCIA comply with prudential regulations, guaranteeing their solvency. Its power of intervention is broad: monitoring financial reserves, overseeing business practices, and imposing sanctions in the event of non-compliance. In addition, the European Solvency II directive imposes strict requirements regarding capital, governance, and transparency. These measures were particularly strengthened in 2025 to address new risks related to, for example, cyberattacks or the effects of climate change. All this is to ensure that each insurer can meet its commitments, even in extreme situations. Strict compliance with these rules is the key to lasting stability in the insurance sector, particularly for players like GROUPAMA and GENERALI, which have a reputation to uphold. Essential Operations and the Diversity of Insurance Products

Insurance companies aren’t limited to simply covering a single type of risk. Their strength lies in the diversity of their products, which cover all aspects of personal and professional life. Here’s what you typically find:

🩺 Health insurance — supplemental or primary, to cover medical expenses.

- 💼 Life insurance — ideal for preparing your estate or guaranteeing an income for your loved ones.

- 🚗 Car insurance — mandatory, with options to also cover property damage or bodily injury.

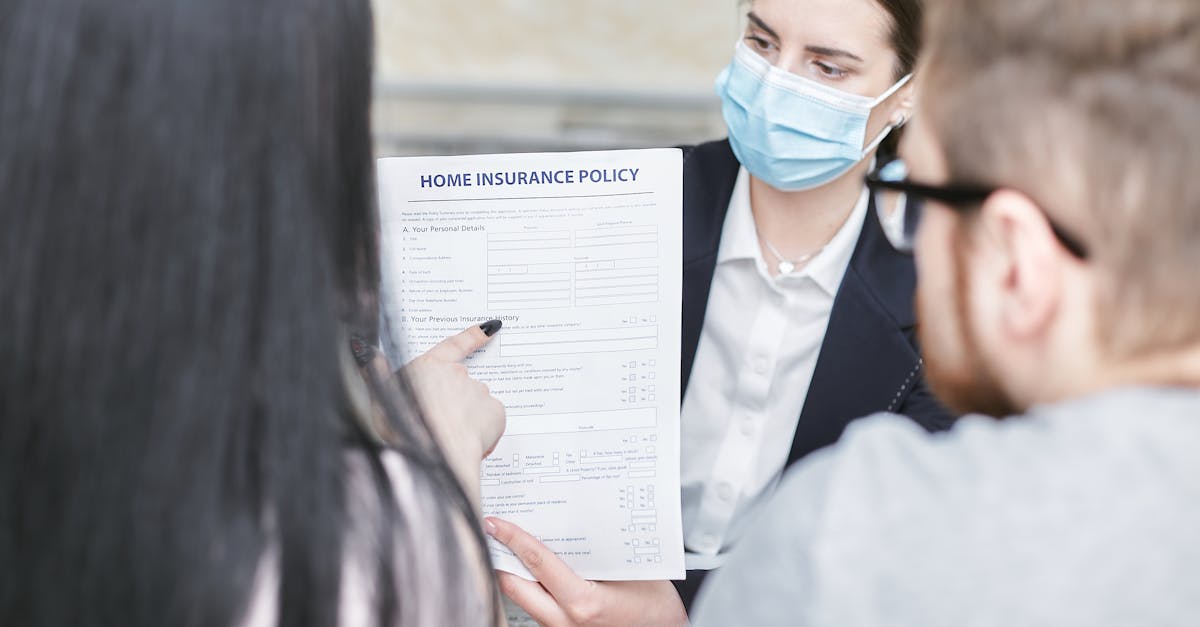

- 🏠 Home insurance — to protect your home against fire, theft, or natural disasters.

- 🔧 Professional insurance — to secure business activity and limit civil liability.

- These offerings are constantly being updated. For example, in 2025, we’ll see the emergence of products such as cyber insurance for SMEs and guarantees for connected devices. The key for an insured is to perfectly target their needs, taking into account their specific risks. Most companies, such as ALLIANZ or MACIF, offer online tools to simulate their guarantees and better understand how they work. This is becoming essential given the growing complexity of modern risks, where prevention is becoming as important as coverage.

Moreover, financial management doesn’t stop there. Insurers must also manage their asset portfolios to meet these obligations. Whether in government bonds, real estate, or even riskier but potentially more rewarding investments like stocks, they must balance risk and return. Geographic and sector diversification has become strategic, especially in 2025 in the face of global uncertainties. Some insurers, such as FONCIA and SMACL, are playing this card by investing in renewable energies or technology, thus ensuring their resilience.

https://www.youtube.com/watch?v=OgXNoUZsuOw Reinsurance: A Lever for Increasing Capacity and Security To address exceptional risks or massive losses, insurance companies resort to a practice called reinsurance. It allows them to transfer part of the risks to other players, such as major global reinsurers. This is often essential for insuring large areas or responding to major natural disasters. For example, a company like ALLIANZ could cover a large number of claims related to a storm in Europe by sharing the risk with other insurers. Reinsurance also offers the opportunity to mitigate the volatility of financial results—essential for long-term stability.

🤝 Proportional reinsurance—sharing risks equally.

🌍 Global diversification—by partnering with international reinsurers.

These risk transfer strategies have enabled the entire sector to evolve smoothly in the face of rising climate and technological challenges. Reinsurance ultimately provides enhanced security for everyone, including companies like GROUPAMA and MACIF, which see it as a strategic management tool.

- Market Innovations and Trends in 2025: A New Era for Insurance

- The insurance sector is not being left behind by the digital revolution. In 2025, players like FONCIA and SPOLEA have developed ultra-modern online services, facilitating underwriting, management, and claims reporting. Insurtechs are emerging with personalized offers based on artificial intelligence. For example, telematics in car insurance or connected health. Moreover, in the face of climate change, many companies are investing in products related to environmental prevention—think renewable energy insurance or flood coverage.

- Market consolidation is also continuing. Merging or acquiring, as AXA and GENERALI have done, allows for pooling investments to remain competitive in this constantly changing landscape. At the same time, digitalization fosters more direct, transparent, and, above all, more responsive customer relationships. Managing future risks depends on their ability to innovate, anticipate, and integrate these technological and societal advances.

Discover our insurance services tailored to your needs. Protect your future with tailor-made solutions, dedicated assistance, and competitive rates. Ensure peace of mind today.

Frequently asked questions about insurance company services

What is the primary role of an insurance company?

Its role is to cover risks against the payment of a premium, by compensating for claims covered by the contract.

You need to analyze your needs, compare guarantees and rates, and use the online tools of major companies like ALLIANZ or MACIF.

- What is the difference between mutual insurance and traditional insurance? Mutual insurance is based on solidarity, is non-profit, and has democratic governance. Traditional companies seek profit and may have more hierarchical governance.

- Are companies really regulated? Yes, by the ACPR (French Regulatory Authority for Public Health) and under the umbrella of the Solvency II Directive, to ensure their stability and the protection of policyholders.